Stock Market Investors Need a Different Approach

The Stock Market Risk Dilemma

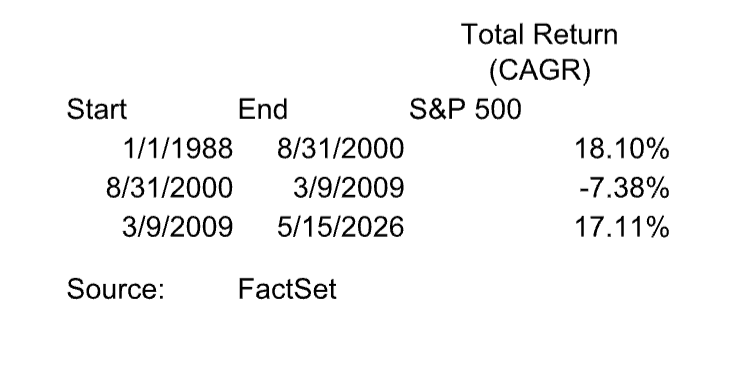

Stock markets have been on an incredible run for a very long time. From its bottom during the Great Financial Crisis on March 9, 2009, the S&P 500 (according to FactSet) has delivered a compound growth rate of 17.11% per year through May 15 th this year. But what will returns look like going forward? I’m not a market timer, but there are warning signs that the next 5-10 years may be a difficult period for investors to navigate. The stock market is eye-wateringly expensive and highly concentrated in a handful of companies. The corporate profits from the AI infrastructure buildout are fragile as long as companies like Anthropic and OpenAI remain unprofitable. In addition, the war in Iran has caused commodity prices to surge which forces inflation higher. How should investors build portfolios now?

Dot Com Comparison

Today’s market environment shares some similarities to the 1990’s. The US was undergoing a massive infrastructure boom to build fiber for another world-changing technology called the internet. That period also experienced incredible returns for the stock market. According to FactSet, the S&P 500 generated a compounded annual return of 18.10% from the beginning of 1988 until the end of August 2000.

We were told the internet would change the world (it did) and that physical stores would soon be gone (according to Statista, more than 83% was still physical as of the 3rd quarter 2025). Internet usage was growing exponentially. The problem, of course, was that fiber was being built even faster, leading to a glut of supply and a series of public company bankruptcies. It was believed that internet traffic was doubling every 90 days, but in fact it was doubling about once per year.

Could the same thing happen with the AI infrastructure buildout? Infrastructure booms are particularly susceptible because the timeline for construction must make predictions into the future. Adoption is eventually slower than anticipated, creating a glut of supply and disastrous economics. America’s pipeline buildout during the mid-2010s is a recent example. Farther back, canals provide a cautionary tale. Not long after, railroads had a similar experience. Here in Indiana, the negative consequences from financing the Wabash and Erie Canal in the 1850’s led to a more conservative fiscal policy that endures today.

When an exuberant stock market is disappointed, the results can be dreadful. From the end of August of 2000 until March 9, 2009, the S&P 500 (according to FactSet) posted compound average returns of negative 7.38%. Investors lost close to half of their money over an almost 9-year period.

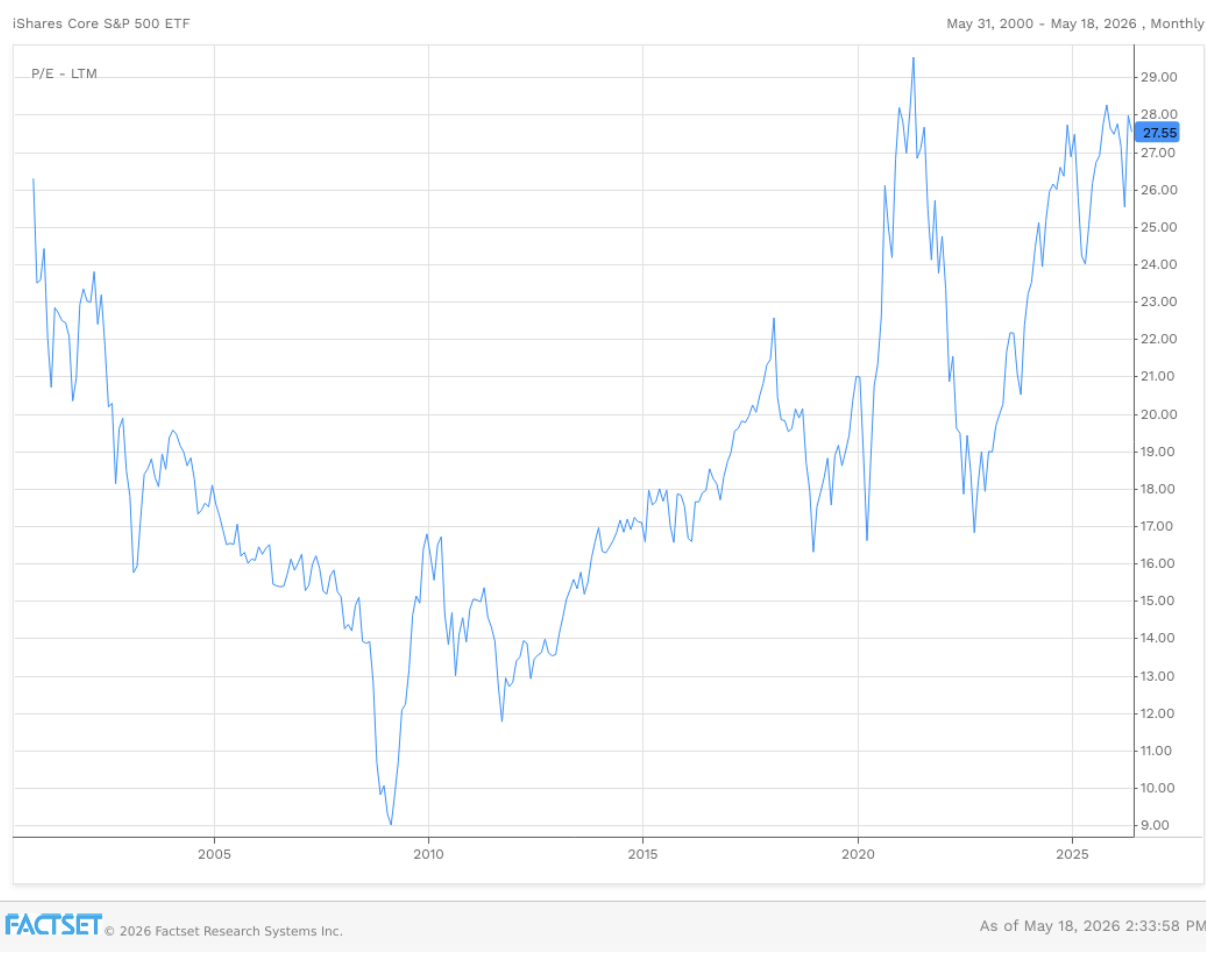

During the height of the dot com bubble, market valuations were extremely high. In fact, the price relative to trailing profits is similar today. Expensive stocks tend to lead to worse investment returns going forward while cheap stocks tend to produce a more favorable result.

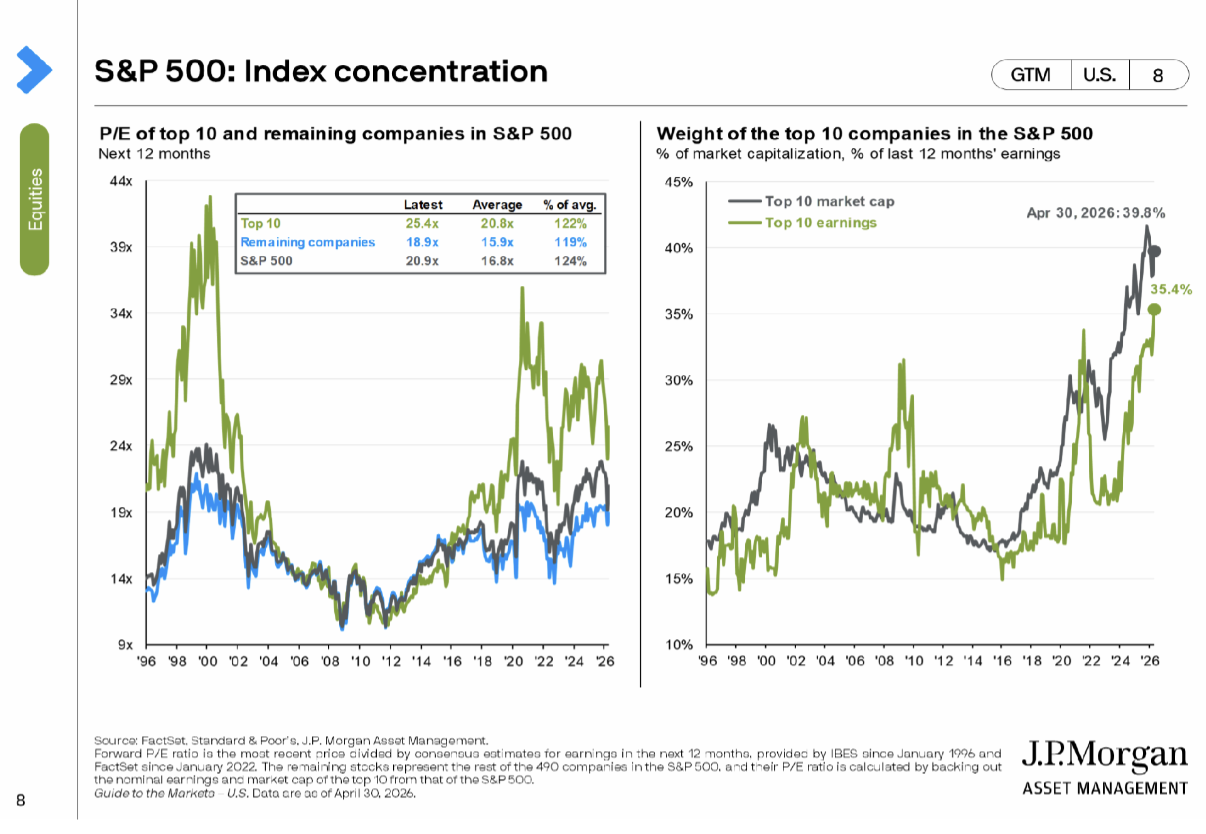

What Options Do Investors Have? - Move Beyond the Tech Sector First off, investors should consider building a more diversified portfolio than the S&P 500 offers. According to JPMorgan (chart below), the largest 10 stocks made up 39.8% of the S&P 500 as of April 30th .

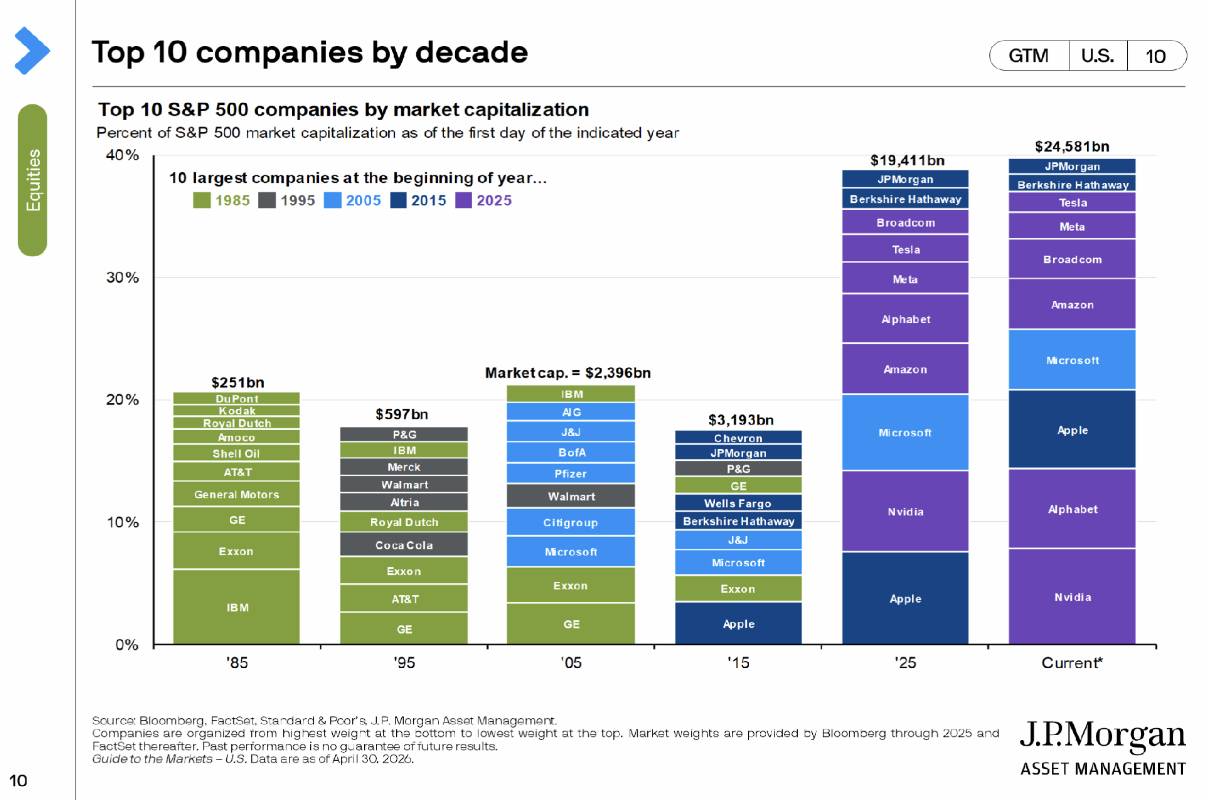

To make matters worse, many of these companies are in similar lines of business. The chart below details how the largest companies change over time. According to FactSet, as of May 15th, the technology sector represented 37.37% of the benchmark while energy made up just 3.4%. That figure likely underestimates technology company influence on the sector as well. Many large “tech” companies are categorized within different sectors. Examples include Tesla & Amazon (Consumer Discretionary), as well as Meta & Alphabet (Communication Services). It is naive to bet so heavily on one economic sector and call it diversified or prudent. At Aurora, we believe investors are better served through a more balanced approach.

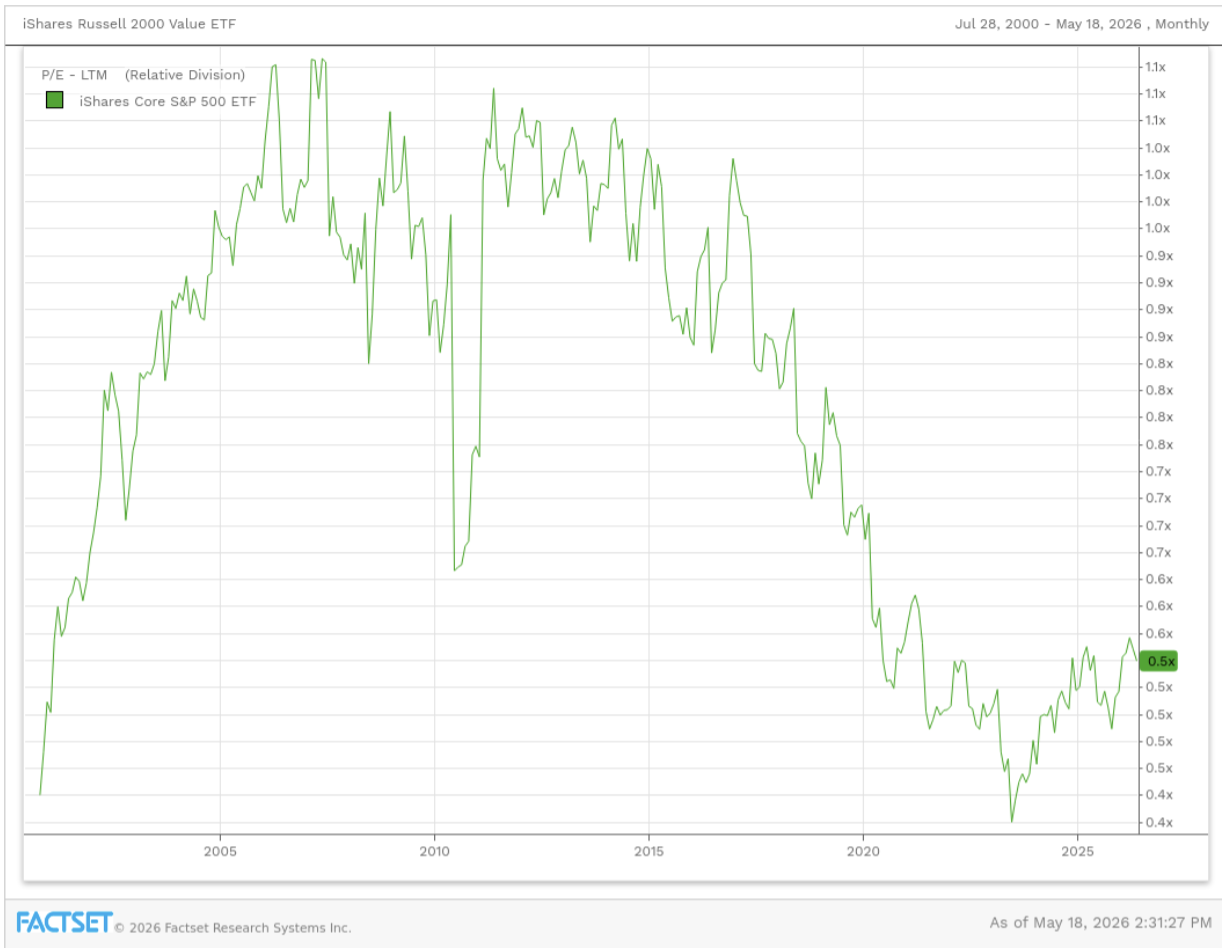

Meanwhile, there are sections of the stock market that offer a considerable discount on a relative basis. “Small Cap Value” stocks as represented by the Russell 2000 Value ETF in the chart below, trade at roughly half the price (relative to trailing profits) as the S&P 500. We haven’t seen this sort of dislocation since...you guessed it...the dot com days.

Where Are We Finding Opportunities – A note on Our Approach

We attempt to build portfolios by purchasing stocks that trade cheaper than our estimated value of the underlying business. On average, that has driven our portfolios towards the stocks of smaller companies. We also believe that energy and defense stocks play an extremely important role in diversification in the current environment. They often perform well when nothing else does. Currently, we see opportunities in many areas where expectations are low (and investors have moved on), like housing, autos, alcohol, software, and wireless telecom services, to name a few.

Benjamin Graham wrote in The Intelligent Investor: “To enjoy a reasonable chance for continued better than average results, the investor must follow policies which are (1) inherently sound and promising, and (2) not popular on Wall Street.”

I’m not sure there’s much wisdom to be found on Wall Street these days, but the S&P 500 sure is popular. We manage 3 equity portfolios (links below) that follow a much different approach to investing relative to the broader stock market, and I’d like to think we follow policies which are inherently sound.

Aurora Asset Management Core Equity

Aurora Asset Management Concentrated Equity

Aurora Asset Management Equity Income

In Summary

We believe the current stock market presents significant challenges for investors. We seek to add value through a differentiated approach. Please reach out to us with any questions. This article represents our thoughts at the time of publication, and we may not update it as our analysis changes. Do your own due diligence and discuss any investment with your financial advisor prior to taking any action.

To learn more about our portfolios and approach, please reach out to us or visit www.auroramgt.com

Invest Curiously,

Austin

Austin Crites, CFA

Chief Investment Officer

Aurora Asset Management/Aurora Financial Strategies

Austin Crites is the Chief Investment Officer of Aurora Asset Management, an Indianapolis-based subsidiary of Aurora Financial Strategies, which is located in Kokomo, IN. He can be reached via email at austin@auroramgt.com. Investment Advisory Services are offered through BCGM Wealth Management, LLC, a SEC-registered investment adviser. Registration with the United States Securities and Exchange Commission does not imply that BCGM or any of its principals or employees possesses a particular level of skill or training in the investment advisory business or any other business. This blog does not constitute advice. This is not an offer to buy or sell securities. Advisor is not licensed in all states. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. BCGM Wealth Management, LLC manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results. Clients may own positions in the securities discussed.