The 3 Concepts Aurora Uses to Guard Against Stock Market Losses

The return of stock market volatility is eliciting questions from investors.

Have you taken on too much risk?

Are you approaching retirement and worried about your nest egg?

Do you have a particularly large investment (as a % of your portfolio) that you are not sure how to unwind?

Nervous about the economy and/or changes in DC?

This article will focus on risks we see in the stock market and a few ways our approach to investing aims to reduce the risk of loss. That said, if you answered yes to any of the above changes then maybe it’s time to revisit your financial plan with your advisor. My partner, Billy Cardwell, shared a similar message here back in 2020.

The Importance of Risk Management

While Albert Einstein called compound interest “the eighth wonder of the world”, Charlie Munger warned to “never interrupt it unnecessarily”. Interruptions can result from large losses in your portfolio. Taking on excessive risk in your portfolio is a bit like trying to sprint through a marathon. The resulting exhaustion can really hurt you down the stretch. Taking risk is a necessary part of investing, but too much can also be a detriment. Do you remember who won the race in the Tortoise and the Hare?

Concerns about the S&P 500

Last month, we discussed our view that the S&P 500 was too expensive, too concentrated, and vulnerable to a trade war. Here’s the link if you’d like to revisit. Before I go further, I’d like to remind readers we are not market timers. The S&P 500 fell over 7% from 02/13 until market close on March 14th so the data in the original post has changed but the overall message remains the same.

In addition to the risks previously mentioned, inflation remains too high for the current interest rate policy and the economic outlook appears increasingly uncertain. I can’t tell you whether the economy will grow or shrink in the coming year. But I can tell you that most economic indicators appear to be weakening. Residential investment, consumer spending and labor markets are all flashing cautionary yellow lights (as of this writing, not panic red in my opinion).

Our Approach to Risk Management

Charlie Munger also said, “All I want to know is where I’m going to die, so I’ll never go there.”

In my observation, the best way to lose a lot of money in the stock market is by simply paying too much. That’s easy to say. But how can we try to avoid this mistake? After all, coming up with a precise valuation on a stock is extremely difficult since we cannot see the future. We use three basic tenants in an attempt to minimize the risk of overpaying.

Demand a Margin of Safety – Ben Graham said it best in The Intelligent Investor, “You don’t try and buy a business worth $83 million for $80 million. You leave yourself an enormous margin. When you build a bridge, you insist it can carry 30,000 pounds, but you only drive 10,000 trucks across it.” Valuation is an imprecise exercise, so give yourself some wiggle room.

Consider the Competitive Advantage (Sustainable Moat) - For most stocks, an estimate of value places significant weight on a forecast of the business. Understanding the durability of a company's competitive advantage(s) (switching costs, cost advantages, network effects, branding, etc.) can help reduce the risk in your forecasts. The weaker the competitive advantage, the less reliable your forecast.

Look for Sensible Corporate Governance/Alignment of Interests – To quote Munger again, “Show me the incentive, and I will show you the outcome.” Misaligned incentives tend to get in the way of a company’s progress and lead to missed business opportunities. It doesn’t matter what boat you are in, if everyone is rowing in different directions, you'll find it difficult to reach your destination.

Does History Support these Ideas?

1.) Demand a Margin of Safety - Stocks that are popular with investors tend to have grown quickly and sport high valuations. “Growth investing” has also seen strong returns in recent years. Indeed, as the chart below shows “growth stocks” have trounced “value stocks” for about the past decade as a result of rising valuations for growth stocks. This has a led to a difficult investment environment for those that are sensitive to price.

Source: FactSet

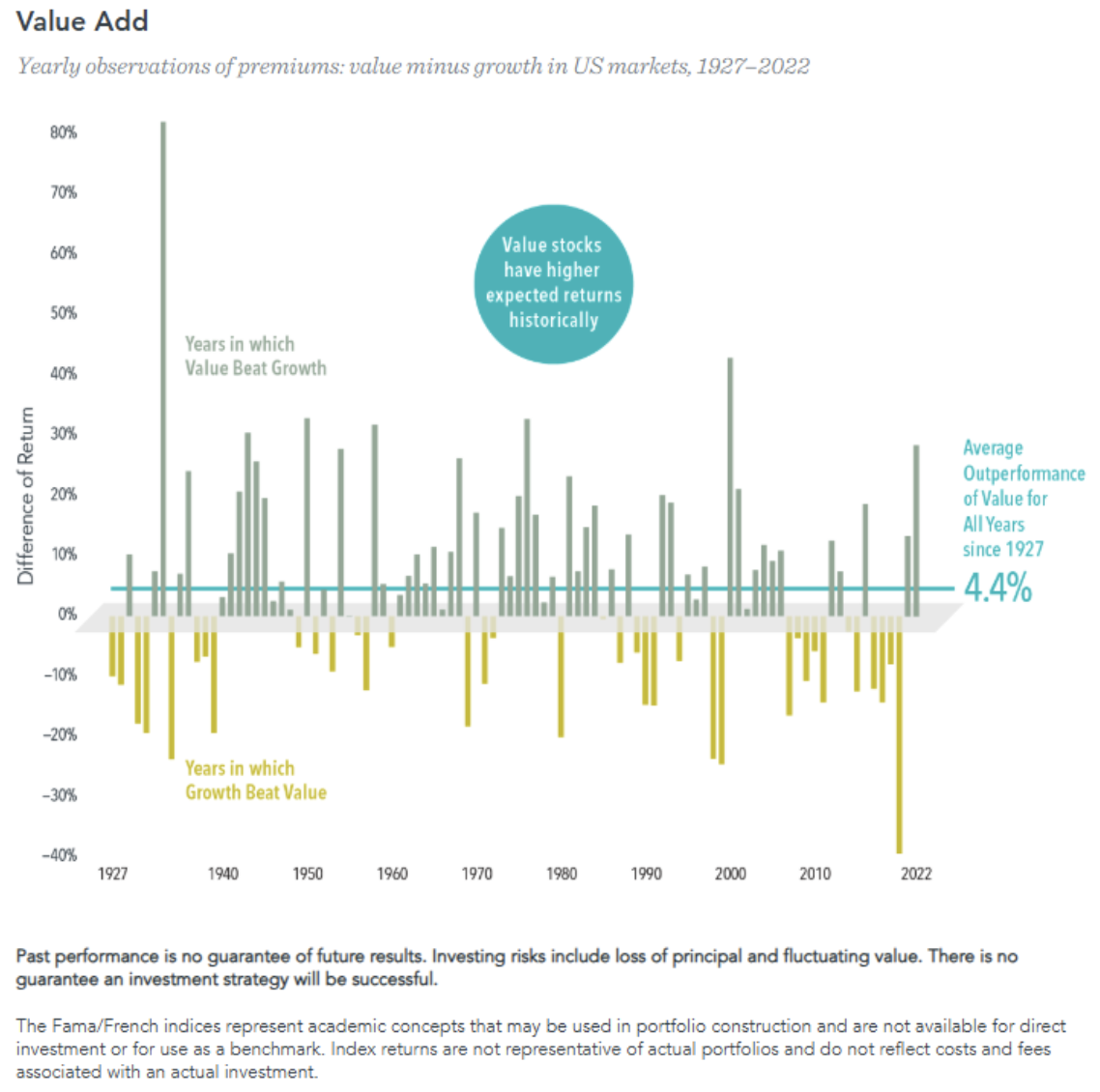

But what about the long term? DFA studied this question and concluded that “value” stocks have outperformed “growth” stocks by an average of 4.4% per year from 1927 to 2022.

Source: DFA

The reason for this phenomenon boils down to investor psychology. Over the long run averages, a “value stock” is more likely to have a margin of safety because low expectations for the business tend to be built into the stock price. Low expectations are easier to surpass. “Growth stocks” tend to have high expectations. They sell at high prices relative to the level of assets and profits and as a result are less likely to have a margin of safety. If those high expectations are not met, the share price can fall dramatically. While everyone remembers companies that succeeded like Amazon, they often forget about the ones that didn’t Pets.com, Webvan, Boo.com, Worldcom, Global Grossing. Should I keep going?

2.) Competitive Advantages are a bit more intuitive. A company with a competitive advantage is more likely to survive poor economic conditions and so they tend to have less risky investment profiles, all else equal. As competitive advantages tend to make financial forecasts more accurate, the inevitable business surprises (both positive and negative) tend to be less dramatic. Morningstar published a book in 2014 titled “Why Moats Matter”. An evaluation of a moat is subjective so there is less history to evaluate, but they began publishing moat ratings back in 2002. From 2002 through 2013, they found that more durable economic moats (competitive advantages) were associated with less volatile stock prices. According to the study and measured by monthly standard deviation of returns: Wide Moat stocks exhibited a 6.9% standard deviation; Narrow was 8.7% and those with No Moat at 13.2%. I would encourage those interested in learning more about stock investing to give the book a read through. Some of the examples are a bit dated now, but the concepts are timeless. As mentioned before.

3.) As a proxy for corporate governance/alignment of interests, let’s consider dividends. Dividends are a method companies use to distribute profits to shareholders. Most investors assume that dividend stocks are relatively less risky and lower return when compared to non-dividend paying stocks. However, that narrative is only half correct. Hartford Funds published a white paper in 2023 studying the risk and return of different buckets of the S&P 500 by dividend policy. Over the 50-year study period, dividend stocks did exhibit lower risk than other stocks as measured by beta and standard deviation. They also earned a higher return for shareholders.

Source: Hartford Funds

While we don’t insist that a stock pays a dividend, we have a preference for them. We look at many other factors including the incentive structure as well as past business decisions. However, we believe a healthy and growing dividend signals a strong business with aligned incentives.

Curious how this approach has worked for us? We publish data on our portfolios at www.auroramgt.com, and you can check out our approach to investing in stocks in more Detail

You may not be ready to ditch your S&P 500 index entirely, but remember, alternatives do exist. There are compelling reasons to think differently at this juncture. At Aurora, we pride ourselves in thinking independently rather than following the herd. We approach investing as buying small stakes in businesses, not as buying and selling ticker symbols on a computer screen. We aren’t trendy. And we like it that way. To learn more about our investment process and thoughts on investing, visit www.auroramgt.com

Invest Curiously,

Austin

Austin Crites, CFA

Chief Investment Officer

Aurora Asset Management/Aurora Financial Strategies