The S&P 500 Dilemma: Overpriced, Non-Diversified, Vulnerable

Most financial advisors would likely agree that clients should own a well-diversified portfolio purchased at reasonable prices. For some time, owning an S&P 500 index fund was a great tool for achieving this as an investor's allocation to stock.

This is no longer true.

The S&P 500 is now:

A concentrated investment in a few large technology stocks

Very expensive relative to historical price-to-earnings ratios

Vulnerable to foreign response in a trade war

If the index did not exist, it would be considered madness to put such a large portion of your eggs in the U.S. technology stock basket at near-record prices. Stay with me until the end, because, luckily, more attractive options do exist. Let’s unpack this.

1. The S&P 500 Is Not as Diversified as You Think

Investors should be shocked to learn that almost 40% of their investment in the S&P 500 is in just 10 stocks. This is not uncommon for active investors who want more exposure to their favorite stocks, but it’s far from ideal for someone seeking broad diversification.

Source: Investing.com

Further, investors may be surprised to learn that their S&P 500 investment is not just concentrated at the holding level but at the industry level. More than 30% of the index’s value is made up of technology stocks—and that actually understates the exposure.

For example:

Amazon (4.4%) is categorized as Consumer Discretionary, but most of its profits come from cloud computing.

Meta (Facebook) (3%) and Alphabet (Google) (4%) are in Communication Services but function as technology companies.

When considering these adjustments, technology exposure exceeds 40%.

Source: FactSet, as of 02/05/2025

2.) The S&P 500 is not reasonably priced

The S&P 500 is at its most expensive level (by forward price to earnings ratio) since the beginning of 2022 and is only eclipsed by the peak of the dot com bubble in 2000. I know, I know. This time is different because AI is going to “change the world”. Do you remember the world pre-internet? No email, no smartphone, no search engine. Did that not change the world? In those days, the frenzy led to a massive overbuild of internet infrastructure. Might that be happening now with AI?

Maybe this time is different, but what if it’s not? What if it’s just the latest iteration of the internet or railroad where the impact on society will be real, but investors are paying too much? Do you want so much of your portfolio riding on this time being different? High valuations tend to precede long periods of overall low returns.

3. Technology Stocks and the S&P 500 Are Vulnerable to a Trade War

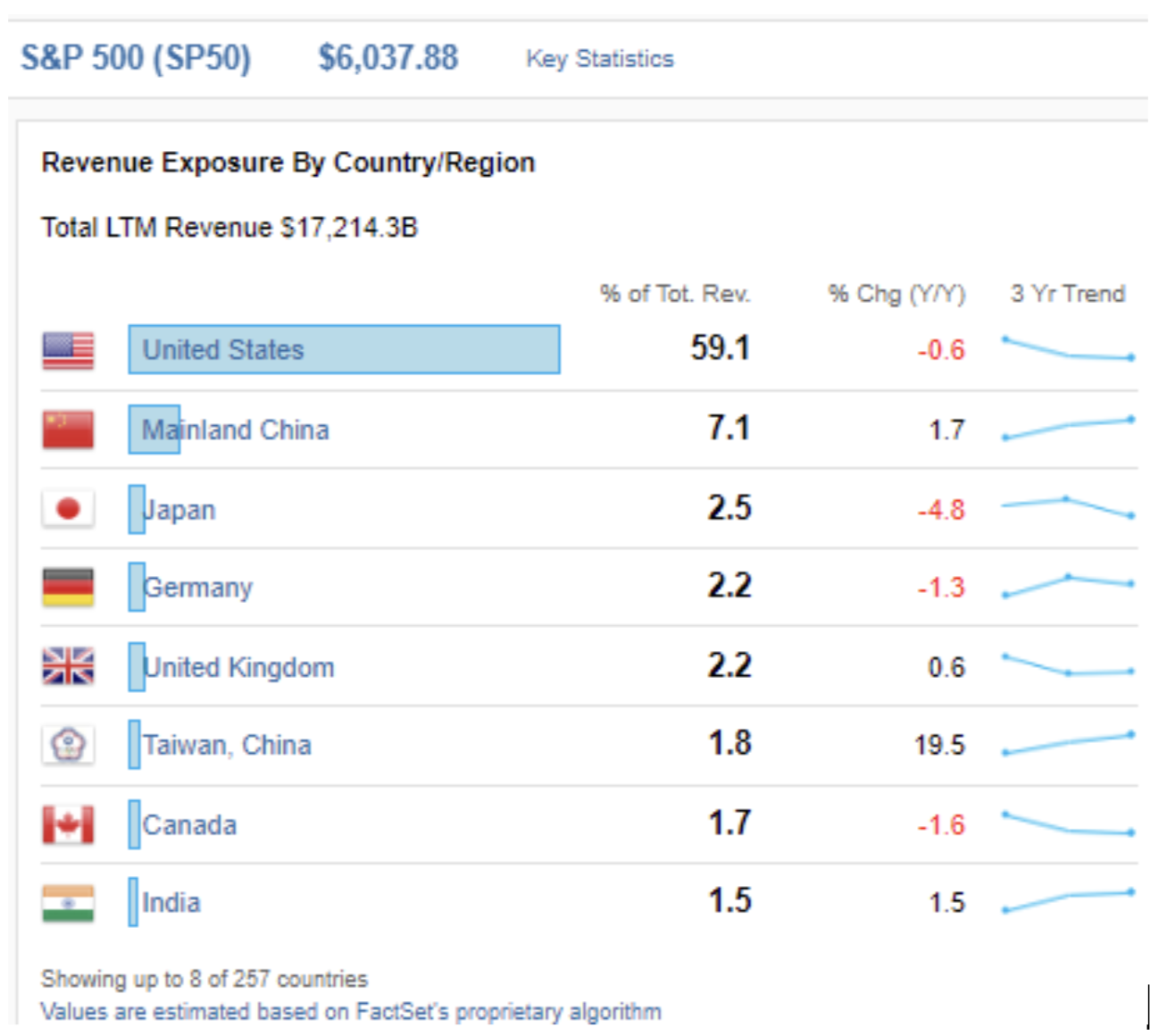

The next 4 years are likely to see a ramping up of trade tensions with the rest of the world. There are pros and con’s to this, but the purpose of this post is not to debate international trade policy. As the US applies pressure to other countries via tariffs, they will need to decide how to respond. The companies in the S&P 500 generate about 41% of their revenue (chart below) outside the United States. High stock prices for these companies are dependent on smooth relations with our largest trading partners.

Source: FactSet as of 02/05/2025

As Fortune points out, China and Europe have already begun targeting US big tech. Let’s look at the largest companies in the S&P 500 and consider the risks.

Apple (about 8% of the S&P 500) generates about 63% of their revenue overseas. Most of their iPhones are assembled in China. If China wanted to hit back, they could cripple the supply chain of Apple.

Nvidia (about 7% of the S&P 500) sources their semiconductors from Taiwan. The US is threatening tariffs on Taiwan. If we place tariffs on those it will drive up the cost to their customers (the largest of which are Microsoft, Google and Amazon).

Tesla (about 2% of the S&P 500) has their most profitable factory in China. If Chinese consumers boycott the American brand or the communist party make life difficult for Tesla as retaliation it would have substantial consequences.

Alphabet (about 4% of the S&P 500) - China recently launched an anti-trust probe into Google (among other US companies). Over half of Alphabet’s revenue comes from overseas and could be a prime target for countries looking to retaliate against tariffs.

It’s Time to Think Differently

Within the US stock market, the best returns over the past decade have occurred within “Large Growth” as stock prices have advanced faster than the profits of those companies. However, companies in the “Small Value” bucket are trading roughly in line with their 20-year historical averages. This suggests a relatively normal future return profile for “Small Value” while the “Large Growth” will likely experience muted returns while their profits catch up to the stock prices. Small cap companies are, on average, cheaper than their larger brethren and have less foreign revenue that could be vulnerable due to geopolitical tensions. Small companies are also much less exposed to the technology industry.

Morningstar recently published a report which included these estimates of asset class returns by Ibbotson. Based on current valuations, they expect foreign companies to outperform US companies by a healthy margin. These stocks can be purchased at more attractive valuations and could benefit if foreign countries wish to support local alternatives, where they exist.

You may not be ready to ditch your S&P 500 index entirely but remember that alternatives do exist. There are compelling reasons to think differently at this juncture. At Aurora, we pride ourselves in thinking independently rather than following the herd. We approach investing as buying small stakes in businesses, not as buying and selling ticker symbols on a computer screen. We aren’t trendy. And we like it that way. To learn more about our investment process and thoughts on investing, visit www.auroramgt.com

Invest Curiously,

Austin

Austin Crites, CFA

Chief Investment Officer

Aurora Asset Management/Aurora Financial Strategies

Austin Crites is the Chief Investment Officer of Aurora Asset Management, an Indianapolis-based subsidiary of Aurora Financial Strategies which is located in Kokomo, IN. He can be reached via email at austin@auroramgt.com. Investment Advisory Services are offered through BCGM Wealth Management, LLC, a SEC registered investment adviser. Registration with the United States Securities and Exchange Commission does not imply that BCGM or any of its principals or employees possesses a particular level of skill or training in the investment advisory business or any other business. This blog does not constitute advice. This is not an offer to buy or sell securities. Advisor is not licensed in all states. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. BCGM Wealth Management, LLC manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results. Clients may own positions in the securities discussed.